Understanding Swift and BIC Codes: Essential Tools for International Payments

In today’s globalized economy, efficient and accurate communication between banks across different countries is crucial. Swift and BIC codes are key in ensuring that cross-border transactions are completed securely and correctly. These codes are part of a sophisticated network that allows financial institutions to exchange information seamlessly, making international payments faster, safer, and more reliable.

In this article, we will explore what Swift and BIC codes are, how they work, and why they are essential for international banking and financial transactions.

What are Swift and BIC Codes?

1.1 What is a Swift Code?

The SWIFT code (Society for Worldwide Interbank Financial Telecommunication code) is an international standard for identifying a specific bank or financial institution in a global financial network. It is used to facilitate international money transfers, ensuring that funds are sent to the correct institution across borders. SWIFT is a messaging network that financial institutions use to exchange transaction information in a secure and reliable manner.

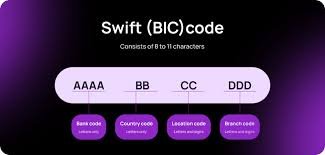

SWIFT codes are often referred to as ISO 9362 codes, after the international standard that governs them. They consist of 8 to 11 characters and can be broken down into several parts, each of which represents specific information about the bank.

Example of a Swift Code:

HSBCGB2LXXX

- HSBC – The bank identifier (HSBC)

- GB – The country code (United Kingdom)

- 2L – The location code (London)

- XXX – The branch code (optional, in this case, it refers to the main branch)

1.2 What is a BIC Code?

The BIC code (Bank Identifier Code) is essentially the same as the SWIFT code. The term “BIC” is sometimes used interchangeably with “SWIFT,” but the key difference is that BIC is the official term adopted by the International Organization for Standardization (ISO). The BIC code is also used to uniquely identify financial institutions globally and facilitates the smooth transfer of funds between banks.

Like SWIFT codes, BIC codes are composed of 8 to 11 characters and follow the same format, consisting of the institution’s name, country, location, and branch information. In fact, BIC is the technical name for what most people call a SWIFT code.

Example of a BIC Code:

HSBCGB2L

- HSBC – Bank identifier

- GB – Country code (United Kingdom)

- 2L – Location code (London)

It’s important to note that although “BIC” and “SWIFT” are used interchangeably, the official term used by ISO is BIC code. However, the term SWIFT code is more commonly recognized in everyday banking.

Structure of a SWIFT/BIC Code

Both SWIFT and BIC codes follow the same format, making them easy to understand and use. A standard SWIFT/BIC code is either 8 or 11 characters long and can be divided into four parts:

- Bank Code (4 characters): The first four letters represent the bank or financial institution. This is usually an abbreviation of the institution's name.

- Country Code (2 characters): The next two letters indicate the country where the bank is located. For example, GB stands for the United Kingdom, US stands for the United States, and DE stands for Germany.

- Location Code (2 characters): The next two characters represent the city or location of the bank. This code helps to identify the specific office or branch.

- Branch Code (3 characters, optional): The last three characters are optional and indicate a specific branch of the bank. If omitted, the code refers to the main office or headquarter branch of the bank.

Example Breakdown of SWIFT/BIC Code:

DEUTDEFF

- DEUT – Bank identifier (Deutsche Bank)

- DE – Country code (Germany)

- FF – Location code (Frankfurt)

If the code includes an additional three characters at the end, such as DEUTDEFF500, it would indicate a specific branch (in this case, branch 500).

Why are Swift and BIC Codes Important?

2.1 Ensuring Secure Transactions

SWIFT and BIC codes serve as a unique identifier for financial institutions, ensuring that the funds are routed correctly to the intended destination. They allow banks to securely and efficiently exchange transaction information over the SWIFT network, reducing the risk of errors and fraud.

Since these codes are standardized, they help streamline international transactions by providing a uniform method for identifying banks, regardless of their location. Without SWIFT/BIC codes, international transfers would be far more complex and prone to mistakes, delays, and fraud.

2.2 Facilitating Cross-Border Payments

International wire transfers can be complicated due to the need to convert currencies, follow different regulatory frameworks, and ensure that funds are sent to the correct bank. SWIFT and BIC codes help to ensure that payments are properly routed across countries, enabling businesses and individuals to send money across borders with ease.

When you initiate an international payment, your bank will use the recipient’s SWIFT/BIC code to identify the correct bank and branch for the transaction. This ensures that funds are transferred directly and accurately, without unnecessary delays or complications.

2.3 Reducing Errors and Miscommunications

By using SWIFT/BIC codes, banks avoid the potential for confusion and errors. These codes are standardized and globally recognized, ensuring that there is no ambiguity when identifying financial institutions. SWIFT codes are particularly important for payments to countries where there are many local banks or institutions, or where there may be language barriers or different alphabet systems.

When transferring large sums of money or dealing with international contracts, any error in the bank’s name or account number can cause significant delays or even result in lost funds. SWIFT and BIC codes minimize these risks.

The Role of SWIFT Network in Global Banking

The SWIFT network (Society for Worldwide Interbank Financial Telecommunication) plays a central role in global banking by enabling secure and encrypted messaging between financial institutions. SWIFT is not a bank itself; rather, it provides a communication platform for banks and financial institutions to transmit information regarding payments, securities, and foreign exchange transactions.

Over 11,000 financial institutions in more than 200 countries rely on the SWIFT network for exchanging financial messages. The network handles millions of transactions daily, processing everything from payments to trade finance, ensuring that banks around the world can exchange financial data quickly and securely.

3.1 How the SWIFT Network Works

When you initiate an international transfer, your bank sends a message via the SWIFT network to the receiving bank. This message contains the recipient’s account information, along with their SWIFT/BIC code, so that the funds can be routed to the correct bank. The SWIFT network verifies and processes the message, ensuring that all information is accurate and secure.

One of the main benefits of using SWIFT is the speed and reliability with which transactions are processed. In addition to SWIFT codes, the network also supports other forms of financial messaging, such as those related to securities, payments, and trade finance. SWIFT messages are encrypted and comply with international security standards, ensuring that sensitive data is protected during transmission.

3.2 Benefits of SWIFT Network for Financial Institutions

For financial institutions, the SWIFT network offers several key advantages:

- Security: The network’s encrypted messaging system ensures that financial data is transmitted securely, reducing the risk of data breaches or fraud.

- Speed: SWIFT messages are processed quickly, allowing international transactions to be completed within hours or days, depending on the payment method.

- Accuracy: SWIFT codes eliminate the possibility of errors in bank identification, reducing the risk of misdirected or lost payments.

- Global Reach: With over 11,000 financial institutions connected to the SWIFT network, banks can communicate with virtually any financial institution worldwide.

How to Use SWIFT and BIC Codes

When sending money internationally, you will often be asked to provide the recipient’s SWIFT/BIC code. Here's how to use these codes to ensure that your transfer is accurate and successful:

- Obtain the SWIFT/BIC Code: The recipient’s bank will provide the SWIFT/BIC code. This can be found on their website, in their account information, or through customer service.

- Enter the Code Correctly: Double-check the code to ensure it is entered correctly. Even a small mistake can cause delays or errors.

- Provide Additional Information: In addition to the SWIFT/BIC code, you will likely need to provide the recipient’s account number, the amount to be transferred, and any other necessary details.

Conclusion

SWIFT and BIC codes are critical components of the global banking system, ensuring that international financial transactions are secure, accurate, and processed quickly. By using these codes, financial institutions can reliably exchange payment instructions across borders, reducing the risk of errors, fraud, and delays.

As the world becomes increasingly interconnected, understanding the role of SWIFT and BIC codes is essential for anyone involved in international finance or payments. Whether you are an individual sending money overseas or a business making cross-border payments, SWIFT and BIC codes are essential tools for ensuring that your funds reach their intended destination safely and efficiently.

In summary, SWIFT and BIC codes are more than just strings of letters and numbers – they are the backbone of international banking, allowing for the seamless movement of money around the world.

What's Your Reaction?

.jpg)

.jpg)